Directors, if your company has outstanding company tax debts that can’t be paid on time or aren’t being paid because they are disputed? Don’t ignore the issue. Address it proactively. Failing to do so is to leave directors personally exposed.

Last financial year the Australian Taxation Office (ATO) issued close to 20,000 DPNs. From 1 July 2023 to February 2024 our practice has already seen over 13,000 DPNs issued and expect to see the total exceed that of previous years. The focus areas are unpaid superannuation, refund fraud, aged debts and audit adjustments.

All indications are that we can expect the firmer approach to continue, the Commissioner of Taxation and Deputy Commissioner having reaffirmed publicly this month that debt remains a high priority and that there will be little room for concession for those that are reactive rather than proactive.

DPNs require immediate attention. Action must be taken within 21 days of the issue date.

Alarmingly, what we have seen in recent times are situations where:

- The debt is over five years old;

- The company has already been deregistered or gone into liquidation; and

- The debt has been paid.

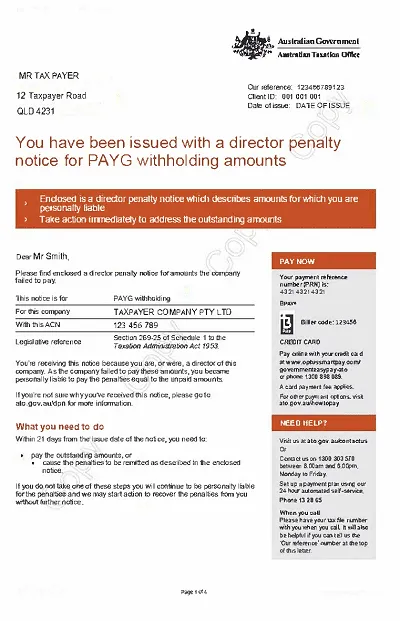

What is a DPN?

A DPN is a notice that the ATO can send to a director of a company making them personally liable for a tax debt and allowing the ATO to take action against the director personally. Importantly the director becomes personally liable upon the issue of the DPN. The type of tax debts of a company for which a notice can be issued are:

- Pay As You Go (PAYG);

- Superannuation Guarantee Charges (SGC); and

- Goods and Services Tax (GST).

It is important to identify the type of DPN issued immediately upon receipt in order to navigate the options for dealing with it as quickly as possible. There are two types of DPNs – a ‘non-lockdown’ DPN and a ‘lockdown’ DPN.

What is a non-lockdown DPN?

A non-lockdown DPN is issued when a company has lodged its activity statements within 3 months of the due date or it lodges the SGC Charge statement within 1 month of the due date but the debt remains unpaid. The debt may not be paid, but importantly, notice has been given to the ATO of the existence of tax debt within the specified period.

A non-lockdown DPN enables a director, within 21 days, to take any of the following actions to discharge the personal liability:

- Pay the debt in full;

- Appoint a voluntary administrator;

- Appoint a small business restructuring practitioner; or

- Appoint a liquidator.

It is not sufficient to simply enter into a payment arrangement to discharge the non-lockdown DPN.

Failure to take one of the above actions within 21 days of the issuance of a non-lockdown DPN will mean the personal liability of the director cannot be thereafter remitted other than by paying the debt in full, or establishing a defence (which are limited).

What is a lockdown DPN?

A lockdown DPN can be issued by the ATO when the company has not notified the ATO of the debt owing within the required timeframes (three months for PAYG and GST, 28 days for SGC) and it has not made payment of the liability.

The only way the lockdown DPN can be complied with is if the company or the director who received the notice pays the debt in full within 21 days of the notice being issued. The failure to comply with the DPN means the liability is “locked down” on the director.

What defences are available to directors?

There are defences to DPN’s where the 21 day period has passed. However these are limited and will very much depend on the facts of each individual case.

There are three defences (one only applicable to SGC and GST) available to directors who have been issued with a DPN. They are:

- That because of illness or for some other good reason it would have been unreasonable for the director to take part in the management of the business. The director does not need to have suffered the illness personally, the illness may be of a close family of the director. It must be shown that the illness or other reason prevented the director from being able to participate in the company’s business.

- The director has taken all reasonable steps to ensure that the company did one of the following:

- complied with paying its tax obligations;

- appointed an administrator;

- appointed a small business restructuring practitioner; or

- commenced winding up.

- For SGC and GST debts only, having taken reasonable care and treating the superannuation or GST legislation as applying to a matter or identical matters in a way that was reasonably arguable.

What happens if I deregister my company? Will I still receive a DPN?

Many directors may think they can simply avoid a director penalty notice by not paying annual ASIC fees and allowing the company to deregister. However, this is not only a breach of the Corporations Act, given that the company has existing debts and liabilities, but it can also lead to serious consequences.

We have seen many directors make this mistake and receive a DPN after the company has been deregistered. The issue is that the company cannot be reinstated in time to address matters such as placing it into liquidation before the non-lockdown DPN expires, which can result in personal liability for the director.

Common mistakes directors believe about DPNs

Here are some common mistakes directors may think about dealing with a DPN

- My accountant said he can get it set aside, this wont work and no accountant can get a DPN set aside. We once had a client who came to us with this exact bad advice and they had to enter into personal bankruptcy, fortunately we saved the family home.

- I can challenge the DPN in Court , to be realistic good luck and be prepared to spend significant money on legal counsel;

- I can change directors or remove myself as a director , this wont work and not only will you still receive a DPN also the new director will incur a DPN as well

What action can the ATO take in regard to an expired DPN?

The other issue that directors should be aware of is that in addition to commencing a proceeding to recover the debt claimed in a DPN, the ATO may also offset the debt against refunds, or retain funds from the taxpayer by garnisheeing funds in their bank account or owed to them by third parties.

Companies, directors, accountants and other advisors need to be aware of the strong action being taken by the ATO at present in regard to the collection of taxation debts.

Corson Fiske can help

If you need advice or guidance to help you navigate your way around the complexities of a DPN then please reach out to our Insolvency and restructuring team. We can help by assessing the available evidence, engaging with the ATO on your behalf and advising you about all options.